Click on the image o view full size

Europe’s largest gambling markets by revenue (GGR).

Italy, Germany, and France dominate in size — but as the map shows, regulation varies significantly between them.

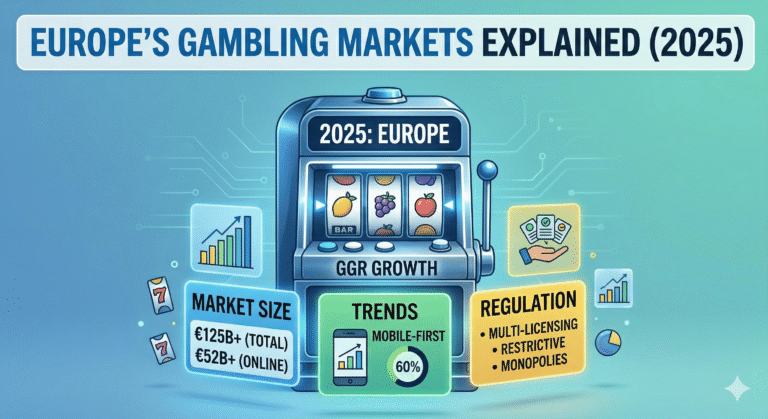

Understanding Europe’s Gambling Landscape

Europe’s gambling markets vary significantly not only in size, but in how they are regulated and accessed by players. While the map above highlights where gambling is open, restricted, or banned, it does not reflect the full economic picture.

Some of the largest gambling markets in Europe — such as France and Germany — operate under strict regulatory frameworks that limit online casino activity. In contrast, smaller markets like Sweden and Denmark provide fully licensed environments with strong digital adoption.

This creates a key distinction:

👉 market size does not equal market opportunity

To better understand this difference, the chart below breaks down the largest gambling markets in Europe by gross gaming revenue (GGR), showing how economic scale compares across countries.

Market Breakdown by Country

🇮🇹 Italy

€21.5B market

Open regulated market

🇩🇪 Germany

€14.4B market

Strict regulation

🇫🇷 France

€14.0B market

Online casinos banned

🇪🇸 Spain

€11.9B market

Open market

🇸🇪 Sweden

€2.5B market

High-growth online market

🇬🇷 Greece

€2.88B market

Regulated with high tax

🇵🇱 Poland

~€2.4B market

Restricted (partial monopoly)

🇵🇹 Portugal

€1.5B market

Regulated market

🇩🇰 Denmark

€1.47B market

Highly regulated & open

🇳🇴 Norway

€1.1B market

State monopoly

🇱🇻 Latvia

€0.30B market

Regulated

🇪🇪 Estonia

€0.06B (tax proxy)

Small regulated market

🇮🇸 Iceland

Small / Restricted

Closed / monopoly system

Key Insights: Europe Gambling Markets in 2025

Europe’s gambling markets in 2025 are often misunderstood when viewed purely through total revenue figures. While headline numbers like Italy (€21.5B GGR), Germany (€14.4B GGR), and France (€14.0B GGR) suggest clear market leaders, the underlying regulatory frameworks reveal a very different picture of real opportunity.

This is why understanding “gambling markets in Europe” requires looking beyond size and focusing on online gambling legality, licensing models, and regulatory openness.

🇮🇹 Italy: Europe’s Largest Regulated Gambling Market

Italy remains the largest gambling market in Europe, with total GGR reaching €21.577 billion in 2024.

The country operates a state-controlled but concession-based system, where private operators can legally offer gambling services under licenses issued by ADM. This includes online casinos, sports betting, and digital gaming platforms, making Italy one of the most important regulated online gambling markets in Europe.

Despite strict advertising restrictions, Italy offers:

- legal online casino operations

- multi-operator licensing system

- strong digital growth potential

👉 This makes Italy one of the best gambling markets in Europe for operators and affiliates

🇩🇪 Germany: Large Market with Heavy Restrictions

Germany is one of the largest gambling markets in Europe, with €14.4 billion GGR in 2024, but it operates under a highly restrictive framework.

Online gambling is legal only under the GlüStV 2021 regulation, which imposes strict rules such as:

- €1 deposit limits per spin

- advertising restrictions

- centralized player tracking systems

While the market is large, these restrictions reduce profitability and limit product flexibility, making Germany a regulated but challenging online gambling market.

🇫🇷 France: High Revenue, Limited Online Casino Market

France presents one of the most important contradictions in Europe. With €14.0 billion GGR, it is one of the largest gambling markets, yet online casinos are banned entirely.

The French market allows only:

- sports betting

- horse betting

- online poker

All under strict supervision of the Autorité nationale des jeux (ANJ).

👉 This makes France a high-value but restricted gambling market, where real iGaming opportunities are significantly limited.

🇪🇸 Spain: Balanced and Licensed Gambling Ecosystem

Spain operates a fully licensed online gambling system, with total market GGR of approximately €11.888 billion in 2025.

The market is split between:

- state-controlled lottery operators

- private land-based gambling

- regulated online operators

Online gambling is legal under the DGOJ framework, but represents only about 12.5% of total market share, showing that Spain is still transitioning toward digital dominance.

🇸🇪 Sweden: Digital-First Gambling Market

Sweden is one of the most advanced online gambling markets in Europe, with total GGR of approximately SEK 28.2 billion (~€2.5B).

Since the 2019 reform, Sweden operates a fully licensed and competitive market, with:

- over 65% of revenue coming from online gambling

- strong player protection systems

- high channelization rates

👉 Sweden represents a high-growth, digital-first market, despite its smaller size.

🇬🇷 Greece: Fast-Growing Regulated Market with High Taxes

Greece recorded €2.8788 billion GGR in 2024, with online gambling accounting for over 37% of the market.

The country operates a mixed model:

- licensed online operators

- state-controlled land-based dominance

However, high taxation (up to ~35% of GGR) makes it a regulated but high-cost gambling market.

🇵🇱 Poland: Restricted Market with State Monopoly Elements

Poland represents a partially liberalized gambling market, where:

- online sports betting is licensed

- online casinos remain a state monopoly

The total market size is estimated at around €2.4B, with strong growth driven by digital adoption.

👉 This makes Poland a restricted but growing iGaming market

🇩🇰 Denmark: One of Europe’s Most Efficient Regulated Markets

Denmark is widely considered one of the most well-regulated gambling markets in Europe, with total GGR of DKK 11.0 billion (~€1.47B).

Key strengths:

- 91.5% channelization rate (very high compliance)

- strong licensing system

- clear tax structure

👉 Denmark is a model regulated online gambling market

🇵🇹 Portugal: High Online Share, Strong Growth

Portugal’s gambling market is heavily online-driven, with total regulated GGR around €1.5B, and online accounting for ~80% of the market.

The market operates under:

- licensed online system

- state-controlled lottery sector

👉 Portugal is one of the fastest-growing online gambling markets in Southern Europe

🇳🇴 Norway: Monopoly Market with High Online Activity

Norway operates a state monopoly gambling system, with total GGR of NOK 12.8B (~€1.1B).

Despite strict restrictions:

- over 75% of gambling activity happens online

- offshore operators still capture significant demand

👉 This creates a high-demand but closed market

🇱🇻 Latvia and 🇪🇪 Estonia: Small but Fully Regulated Markets

Latvia:

- €299.6M GGR (2025)

- fully regulated online market

Estonia:

- smaller market (~€61M tax proxy)

- fully licensed and digital-friendly system

👉 Both countries represent small but accessible gambling markets in Europe

🇮🇸 Iceland: Restricted Market with Offshore Leakage

Iceland operates one of the most restrictive gambling systems in Europe, based on:

- charity monopolies

- general prohibition of commercial gambling

However, demand remains high, with significant activity shifting to offshore platforms.

👉 This makes Iceland a closed but high-interest market

The European gambling industry in 2025 clearly shows that:

The biggest gambling markets are not always the best markets

Countries like France and Germany offer massive revenue potential but impose strict limitations, while smaller markets like Sweden, Denmark, and Portugal provide better regulatory environments for online gambling growth.

For anyone analyzing online casino markets in Europe, the key factor is not just GGR — but regulation, licensing, and accessibility.

he largest gambling markets in Europe are Italy, Germany, France, and Spain. Italy leads with over €21.5 billion in gross gaming revenue (GGR), followed by Germany and France with around €14 billion each. Spain also remains a major market with nearly €12 billion in GGR.

Online casinos are fully legal and regulated in several European countries, including:

Italy, Sweden, Denmark, Spain, Portugal

These markets operate under licensing systems that allow private operators to offer online casino games legally.

In contrast, countries like France and Poland restrict online casino activity, often limiting it to state monopolies or banning it entirely.

France is one of the largest gambling markets in Europe, generating around €14 billion in GGR. However, it does not allow online casinos.

Yes, online gambling is legal in Germany, but only under strict regulation.

Countries with the most balanced and open gambling regulation include: Sweden, Denmark, Malta, Spain